-

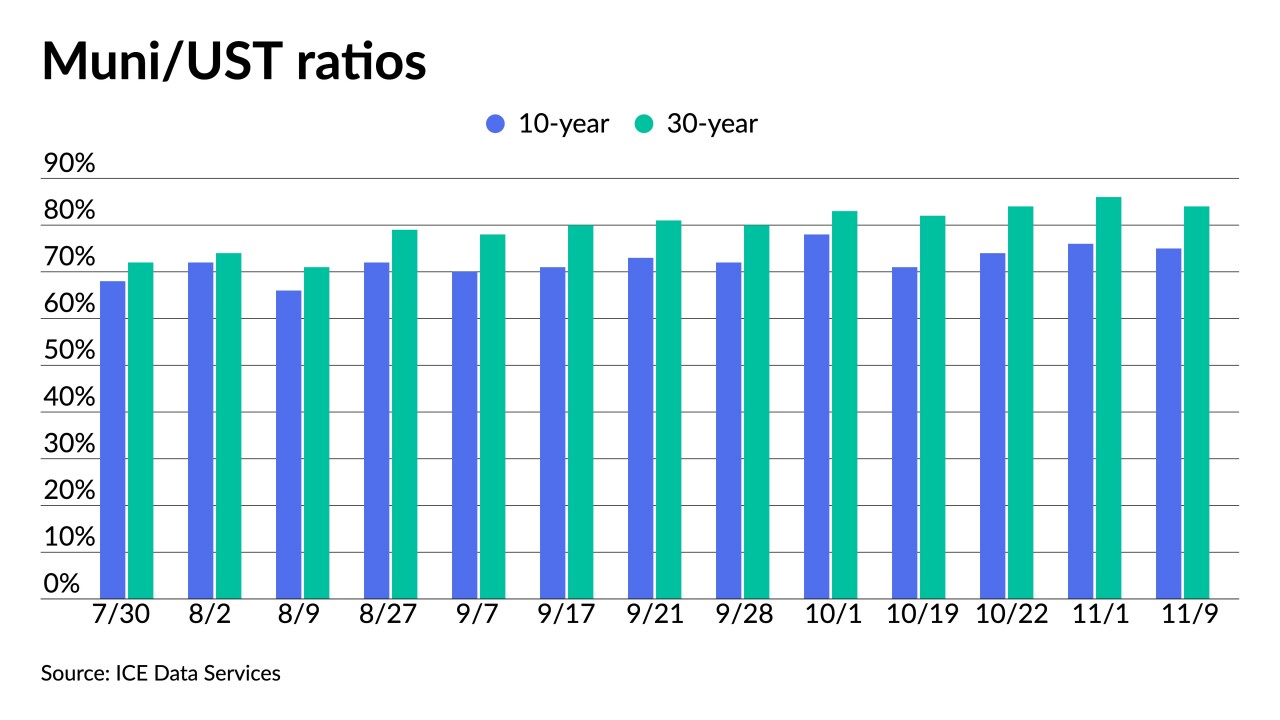

Triple-A benchmarks have fallen double digits since Nov. 1, with the largest moves out long. California, the District of Columbia, Wisconsin and other issuers part of a $6 billion new-issue calendar priced.

November 9

-

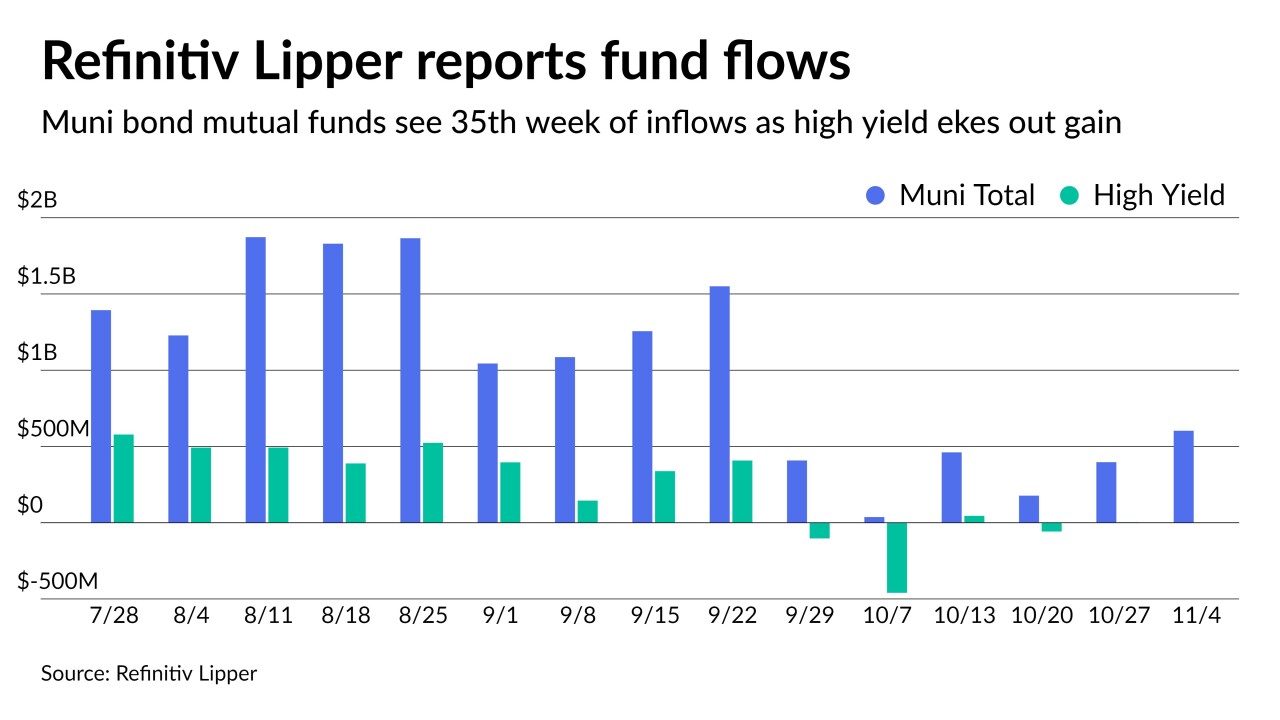

For 35 weeks in a row, investors have put cash into municipal bond funds as Refinitiv Lipper reported $603 million of inflows while high-yield funds eked out a gain of slightly more than $1 million.

November 4

-

The Treasury Department, for the first time in more than five years, will likely unveil a scaling down of its behemoth quarterly sale of longer-term securities.

November 1

-

Without the primary in play and a mostly muted secondary, triple-A yield curves were little changed, coming nowhere near the moves in UST with the 10- and 30-year falling five and six basis points as equities saw their worst day since May.

September 20

-

The U.S. Treasury kept its quarterly auction of long-term debt, planned for next week, at a record size to help fund the government’s continuing wave of stimulus spending.

May 5

-

Exactly one year after record billions were pulled from municipal bond mutual funds and the market was in free fall, municipals followed U.S. Treasuries this week as the markets continued to dismiss the Fed's outlook on inflation and rates.

March 19

-

The Treasury Department’s $60 billion sale of two-year notes on Tuesday broke one of the few remaining records of the low interest-rate era.

February 23

-

With the U.S. Treasury sell off, municipal to UST ratios fell below 55% in 10-years.

February 16

-

Muni yields have been in a nine-basis point range since the beginning of the year while UST yields have fluctuated more than 20 basis points. With so little supply, muni credit spreads continue to compress.

January 20

-

Tax-exempt performance is dependent on what supply looks like versus taxables. The 30-day visible supply shows more than 30% taxables on tap, though some analysts say the taxable increase makes exempts more attractive.

January 19

-

It was inevitable that muni yields would need to rise somewhat as the UST 10-year broke above 1%, however participants said the supply/demand imbalance will keep munis from rising as quickly as Treasuries. More than $1 billion inflows reported.

January 7

-

Dominick D'Eramo, head of fixed income at Wilmington Trust Investment Advisors, talks with Chip Barnett about how the municipal bond market did in 2020 and what may be on tap for munis in the new year. (12 minutes)

December 31

December 31

-

ICI reported another $2.3 billion of inflows, new deals continue the march to lower yields and benchmarks rose a basis point seven years and out for the first time since the beginning of December.

December 16

-

The state of Illinois sold $2 billion of three-year notes to the Federal Reserve's Municipal Liquidity Facility at 3.42%.

December 15

December 15

-

Even with COVID-19-related shutdowns — a New York City lockdown may be imminent — issuers are pricing bonds into an extremely low-rate environment.

December 14

-

Strong technicals, low supply, yield-seekers keep munis outperforming.

December 8

-

The primary's diversity of credits and size relative to November has grown, but it is just not enough to push yields higher as redemptions flood the market. Some analysts still say a mild correction at least is due.

December 7

-

Refinitiv Lipper reported inflows of net $201 million for the week ending Dec. 2, down from $386 million the week prior.

December 3

-

Until supply increases, year-end demand has munis outperforming. ICI reports another multi-billion week of inflows.

December 2

-

Munis are likely to lag Treasuries in some fashion once year-end empathy settles in mid-month and ratios become a factor.

December 1