-

Municipals triple-A benchmarks continue the trend of ignoring other markets to start 2022. The new year will likely usher in slower growth and continued inflationary pressures, analysts said.

January 3

-

Tax risks continue to linger as they are preserved as a potential offset for whatever level of spending all 50 Democratic senators can agree to, but potential approval of the legislation remains a question mark.

December 22

-

Municipal market participants need to be vigilant in monitoring liquidity and the impact of growing inflation.

December 22 ArentFox

ArentFox -

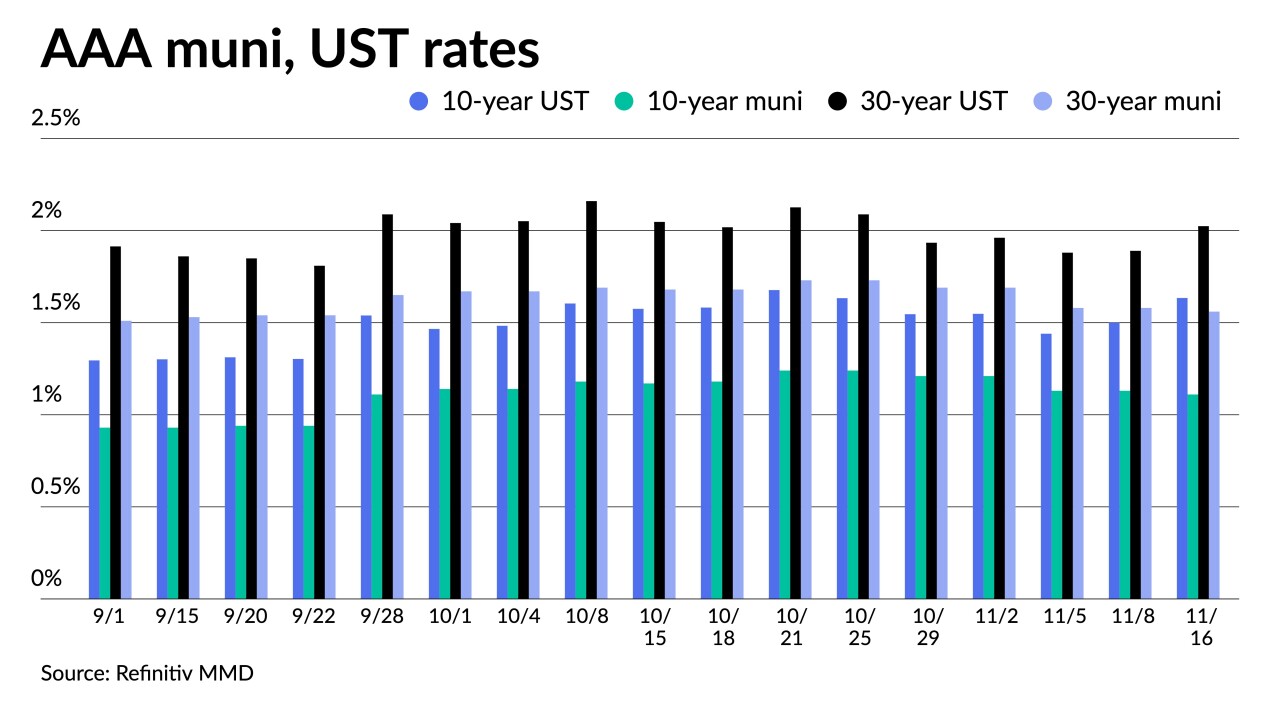

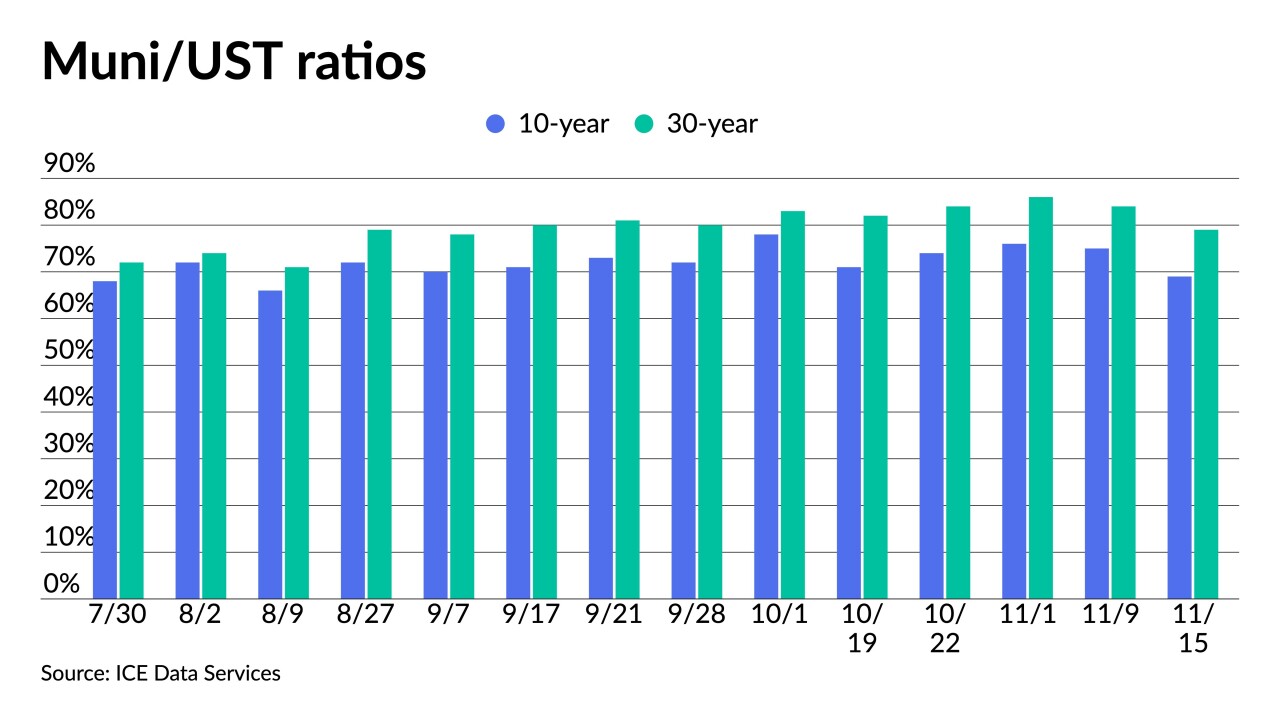

U.S. Treasuries saw losses pushing municipal to UST ratios on the 10- and 30-year lower again.

December 21

-

The Build Back Better in its current form essentially has been killed by Sen. Joe Manchin, likely limiting the potential for tax hikes in the coming year.

December 20

-

Despite outside pressures, municipal fundamentals are strong with improving credit pictures, issuers flush with federal cash and the ongoing supply-demand imbalance.

December 16

-

Triple-A yield curves were unchanged on the day and mostly have not budged but a basis point in spots since the end of November.

December 14

-

There are $8.127 billion of negotiated deals on tap and a mere $367.4 million of competitive loans slated, none over $100 million. Thirty-day visible supply totals $9.9 billion and net negative supply is at $8.4 billion.

December 10

-

The Investment Company Institute reported $289 million of inflows into municipal bond mutual funds in the week ending Dec. 1, down from $965 million in the previous week.

December 8

-

Thirty-day visible supply drops to $13.54 billion with still a large chunk of new issues to be priced Wednesday and Thursday.

December 7

-

The Investment Company Institute reported $974 million of inflows into municipal bond mutual funds in the week ending Nov. 23, down from $1.430 billion in the previous week.

December 1

-

Powell says the FOMC will consider ramping up tapering when more information about Omicron and its impacts are known, further flattening the UST yield curve.

November 30

-

Rising rates and rising inflation are key concerns for municipal bond buyers.

November 30

November 30

-

Economists appear to be less concerned about Omicron, with some saying that even if the variant causes another pandemic wave, it is more likely to "slow rather than interrupt" the global economic recovery.

November 29

-

Former U.S. Treasury Secretary Lawrence Summers said Federal Reserve policy makers are signaling a “new era” in which they recognize the U.S. economy is overheating as inflation runs at its fastest in three decades.

November 24

-

With the leadership questions mostly answered, the Fed must figure out what to do about inflation. The markets expect the Fed will have to raise rates sooner than planned, and perhaps speed up taper to do so.

November 23

-

A large new-issue calendar began pricing in the negotiated and competitive markets, with a few deals bumped off the day-to-day calendar.

November 16

-

State economies are generally stronger than anticipated in the first half of 2021.

November 16

-

Outside influence "beyond the control of the muni bond market" is needed to derail the recent positive momentum.

November 15

-

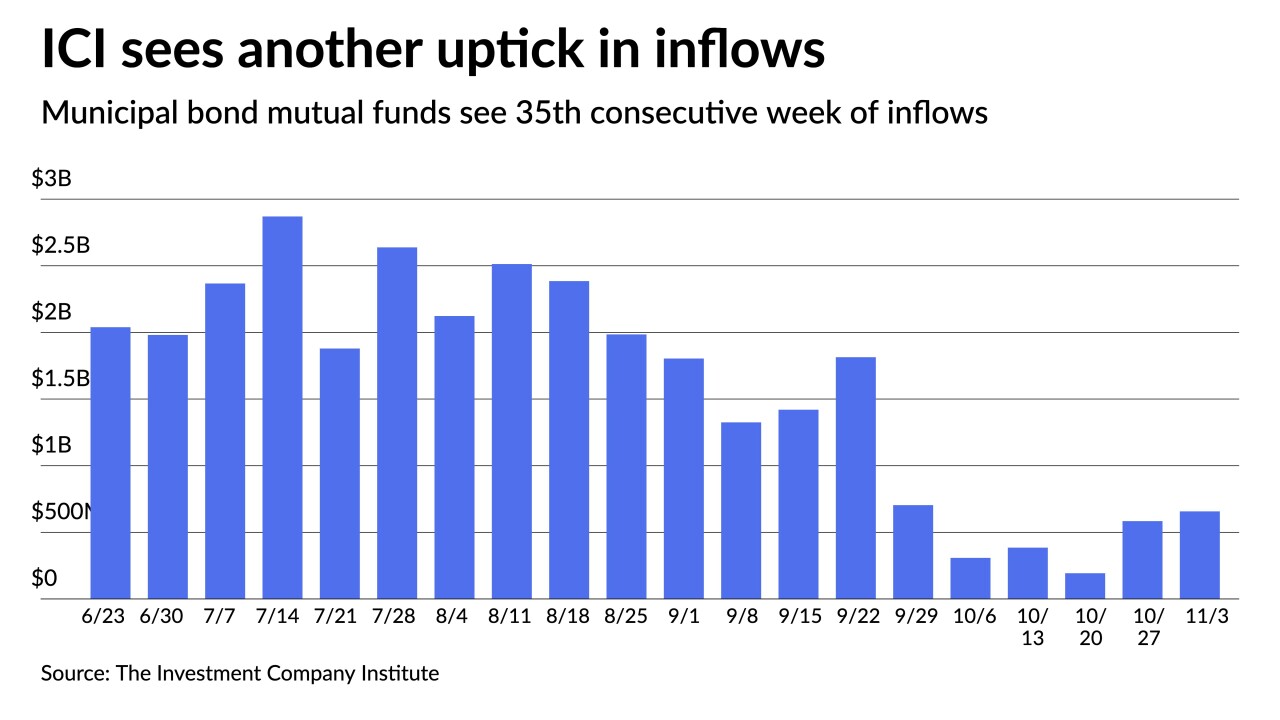

The Investment Company Institute reported $657 million of inflows into municipal bond mutual funds while ETFs saw $828 million of inflows, a massive increase over the $43 million reported a week prior.

November 10