-

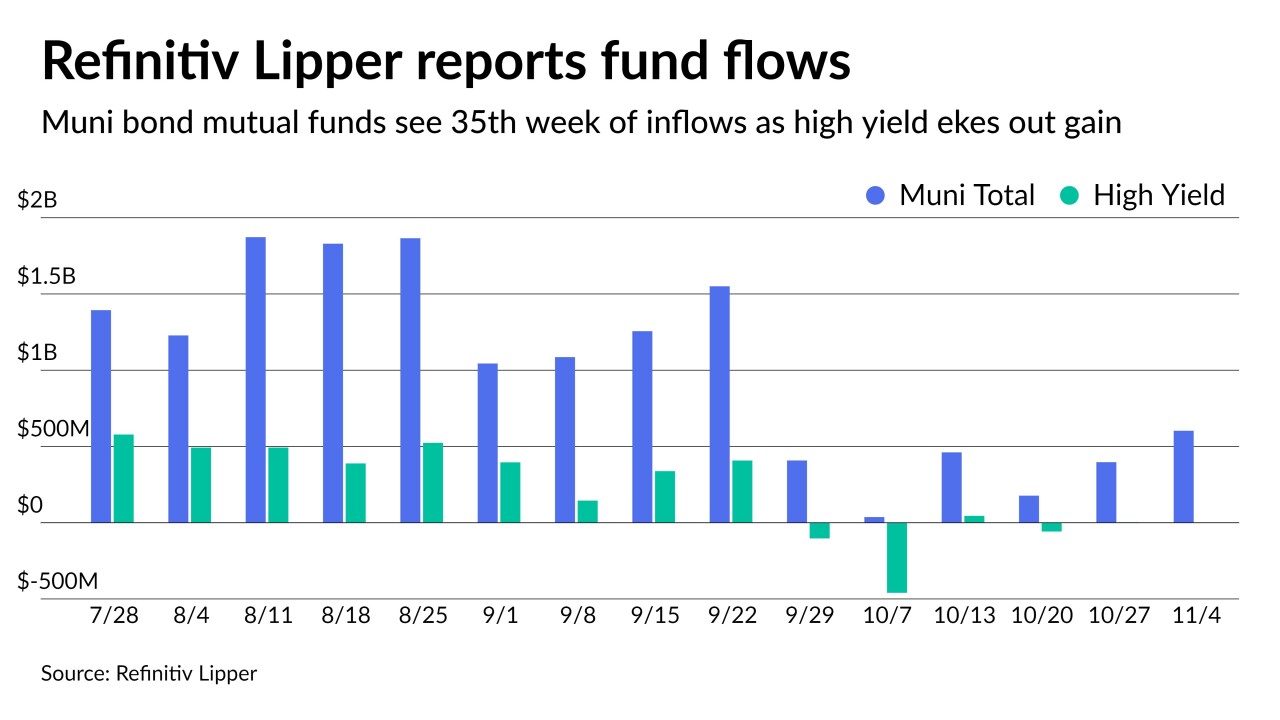

For 35 weeks in a row, investors have put cash into municipal bond funds as Refinitiv Lipper reported $603 million of inflows while high-yield funds eked out a gain of slightly more than $1 million.

November 4

-

After the FOMC made taper official, high-grade benchmark yields ended the day one to three basis points better while USTs ended the day higher after an up-and-down trading session that moved the 30-year back above 2%.

November 3

-

The FOMC will likely take the opportunity to profess its reliance on data to decide liftoff and reiterate the threshold for a rate hike remains higher than for taper.

November 2

-

Though monetary policy has been in the forefront, at mid-month the tone changed with global inflation outlooks and federal infrastructure and social package in flux.

November 1

-

A lighter, $5 billion calendar, heavy on healthcare, kicks off November. Most participants agree volatility in U.S. Treasuries will be a leading factor for municipal market performance. Uncertainty in Washington also isn't helping the asset class.

October 29

-

ICI reported the lowest inflows since outflows in March, while exchanged-traded funds saw an uptick.

October 27

-

As of now, returns for the month will very likely end in the red. The Bloomberg U.S. Municipal Index is at -0.40% for the month and +0.39% for the year.

October 26

-

Jeffrey Cleveland, chief economist at Payden & Rygel, discusses the Federal Reserve’s upcoming meeting, inflation, what taper will mean, when the Fed might decide to lift off, and possible leadership changes. Gary Siegel hosts. (30 minutes)

October 26

-

Municipal bond mutual fund inflows fell to $177 million while high-yield is back to outflows, both signaling selling may be moving the market toward another larger correction.

October 21

-

The $1 trillion spending bill could boost GDP by 0.2% by 2031.

October 21

-

Spreads have been widening, but secondary trading was on the light side and triple-A benchmarks were cut by only a basis point in spots even as U.S. Treasury yields once again rose on the 10- and 30-year.

October 19

-

Municipals have mostly held steady as bid-wanteds have risen, but so have yields and ratios, making for a more satisfactory range for investors getting into the market at these new higher levels.

October 14

-

Volatility in the U.S. Treasury market continues to pull on municipal bond valuations, despite little trading volume.

October 12

-

CB President Christine Lagarde said Wednesday that inflation “is largely attributable to the reopening of the economy.”

September 29

-

Large new issues from California, New York utilities and airport deals were repriced to lower yields and remained the focus for the municipal market, again ignoring a swing by U.S. Treasuries.

September 14

-

Refinitiv Lipper reported $1.1 billion of inflows into municipal bond mutual funds, with high-yield falling to $144 million. Even with the lower reported inflows, funds still raked in record billions so far in 2021.

September 9

-

COVID has impacted so many sectors of life over the past two years. Its presence has spiked a sudden increase in inflation, and whether it is a blip or a long-term trend is still unknown.

August 25 tru Independence

tru Independence -

Treasury Secretary Janet Yellen said that by the end of this year, monthly price changes will be running at a level consistent with the Federal Reserve’s target, even if year-over-year numbers continue to show uncomfortably high inflation.

August 4

-

Joe Kalish, chief global macro strategist at Ned Davis Research, discusses his thoughts on when the Federal Reserve will announce it will cut back on its asset purchases, the possibility of Chair Jerome Powell’s re-nomination and what to expect from the Jackson Hole summit. Gary Siegel hosts (27 minutes)

August 3 -

Fundamentally, much of the price inflation we’ve experienced over the past year can be attributed to the trillions of dollars of new money pumped into the economy that’s been looking for a home ever since.

July 27 MaxMyInterest

MaxMyInterest