-

Muni performance has been strong as of late, and spreads have actually corrected after a month of gradual widening.

March 21

-

Next week's potential volume is slated to be $7.7 billion. The largest deal of the week comes from New York City with $891 million of tax-exempt general obligation bonds. Recent New York paper traded up Friday.

March 18

-

The MSRB has issued a warning that with the rise in interest rates in recent months, bonds trading at a discount may be less liquid than those trading at par.

March 18

March 18

-

With volatility and illiquidity realities for the foreseeable future, insights into new-issue and secondary pricing are critical.

March 18 Lumesis

Lumesis -

Outflows continued, rising significantly in the latest week, with Refinitiv Lipper reporting $2.136 billion coming out of municipal bond mutual funds, following outflows of $661.675 billion in the previous week.

March 17

-

The Investment Company Institute on Wednesday reported $2.258 billion of outflows in the week ending March 9, down from $3.502 billion of outflows in the previous week.

March 16

-

Bond investors are understandably cautious in response to recent market volatility and ahead of what is expected to be a Fed rate hike Wednesday, participants say.

March 15

-

As 2022 unfolds, a confluence of challenges has affected pricing, trading and fund flows in the muni market.

March 15

March 15

-

The market is being driven by the prospect of higher long-term inflation and the potential that the Federal Reserve may have to raise rates further than expected.

March 14

-

DASNY leads the calendar with $2.3 billion of exempt personal income tax bonds and $662.32 million of taxables. Potential volume is slated to be $5.11 billion, with $4.392 billion of negotiated deals and $718.1 million of competitive loans.

March 11

-

Outflows continue but dropped significantly in the latest week with Refinitiv Lipper reporting $662 million of outflows from municipal bond mutual funds following $2.823 billion the week prior.

March 10

-

The Investment Company Institute on Wednesday reported another round of large outflows, this week at $3.502 billion, up from $2.647 billion of outflows in the previous week.

March 9

-

Secondary trading showed weaker prints, moving triple-A yields higher by three to seven basis points, outperforming larger losses in UST. California priced $2.2 billion of GOs for retail.

March 8

-

As municipals continue to underperform the moves in U.S. Treasuries, current ratios are attractive and present a buying opportunity.

March 7

-

Market volatility has risen significantly, particularly in the last several weeks, with daily Treasury yield swings of 10 basis points or more becoming the norm with municipals struggling to stabilize.

March 4

-

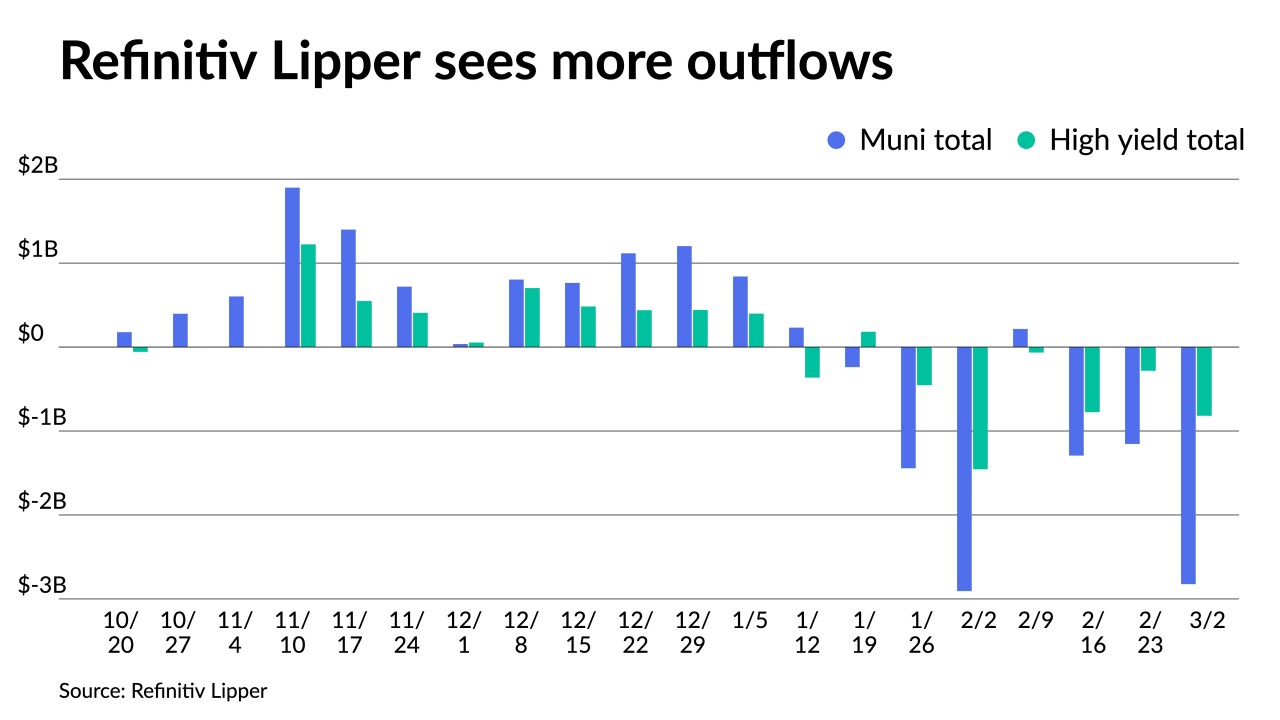

Ongoing turmoil in the Ukraine is roiling markets, municipals included. Refinitiv Lipper reported more outflows, with high-yield seeing $818.218 million pulled out in the latest week.

March 3

-

The MSRB’s annual fact book, released on Wednesday, shows that par amount trading volume was down 28% in 2021 when compared with 2020.

March 3

-

The Investment Company Institute on Wednesday reported $2.637 billion of outflows in the week ending Feb. 23, down from $3.120 billion of outflows in the previous week.

March 2

-

The Russian invasion of Ukraine could slow interest rate hikes and has led the market to pull back on the chances of a 50-basis-point liftoff.

March 1

-

All markets, but particularly municipals, are in uncharted territory once again, with volatility amplified by the crisis in Ukraine and a still somewhat uncertain path for the Federal Reserve and inflation.

February 28