-

"We're navigating a crosscurrent of macro risks — tariffs, tax policy proposals, DOGE cuts, and evolving economic data — layered on top of a broader risk-off tone," said James Pruskowski, CIO of 16Rock Asset Management.

March 26

-

What's happening to the muni market is the "confluence of modest selling (via fund outflows and retail perhaps pausing during tax season); a heavy new issue calendar; and very thin near-term reinvestment expectations," said Matt Fabian, a partner at Municipal Market Analytics.

March 25

-

Lighter supply, at an estimated $7.9 billion, and still-attractive valuations should allow for solid muni performance this week, said J.P. Morgan strategists.

March 24

-

Municipal bond issuance for the week of March 24 is at $7.923 billion, with $6.673 billion of negotiated deals and $1.251 billion of competitive deals on tap.

March 21

-

Separately managed accounts have exploded in the muni market in recent years but high-yield SMAs remain rare.

March 21

-

Most of Thursday's issuance came from competitive deals, the largest being the Dormitory Authority of the State of New York with $2 billion-plus and California with $889 billion.

March 20

-

Wednesday marked the first trading session that saw cuts more than a basis point or two in spots since last week's extended selloff.

March 19

-

"While there has been some reported buying by relative value institutions amid higher ratios from the muni-centric price correction, the market as a whole may not rally this week," said Matt Fabian, a partner at Municipal Market Analytics.

March 18

-

Municipals are little changed to start the week after last week's selloff, which saw muni yields cut up to 20 basis points out long.

March 17

-

March had been expected to be difficult due to a "combination of heavy supply, low redemptions, rate volatility, tax-related selling and now fund outflows," said Barclays strategists Mikhail Foux and Grace Cen.

March 14

-

After digit-double cuts out long Wednesday, muni yields rose an additional two to four basis points, depending on the curve, on Thursday.

March 13

-

"The supply/demand dynamic is a headwind for the muni market this week as supply is expected to be elevated," said Cooper Howard, a fixed income strategist at Charles Schwab.

March 12

-

"The ever-shifting narrative regarding President Trump's tariff policies is throwing fuel on the fire of unpredictability," said SWBC's Chris Brigati.

March 11

-

The market rally "took a bit of a breather last week, with yields rising across the curve," said Daryl Clements, a portfolio manager at AllianceBernstein.

March 10

-

"March is not an overly positive month for munis, but a lot will depend on U.S. Treasuries," said Barclays strategist Mikhail Foux.

March 7

-

"Markets fixate on one risk at a time, and there's no shortage right now. Volatility has spiked, liquidity is thin, and buyers are sidelined — but that's temporary," said James Pruskowski, chief investment officer at 16Rock Asset Management.

March 6

-

Issuance remains heavy this week, but while it's elevated, the muni market is "structurally undersupplied," meaning if 2024's record level of $500 billion-plus of issuance was doubled, the market could still digest it quite well, said Wesly Pate, a senior portfolio manager at Income Research + Management.

March 5

-

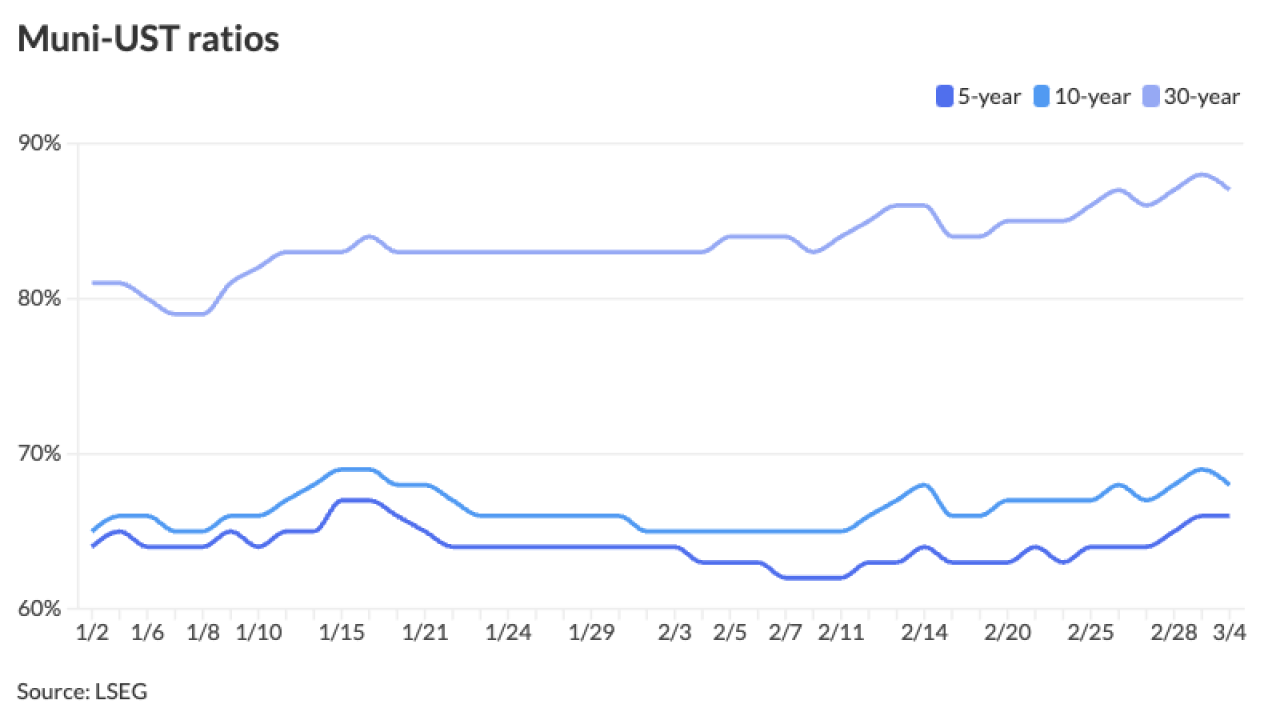

Short-end U.S. Treasuries rallied mid-morning, while UST yields were little changed out long, but ended the day weaker across most of the curve with the greatest losses out long. Munis were steady throughout the day.

March 4

-

"Apathy and caution" were the theme of the past week, said Birch Creek strategists.

March 3

-

The Trump administration wants to shed federal office space, and bonds backed by those leases are feeling the heat.

March 3