-

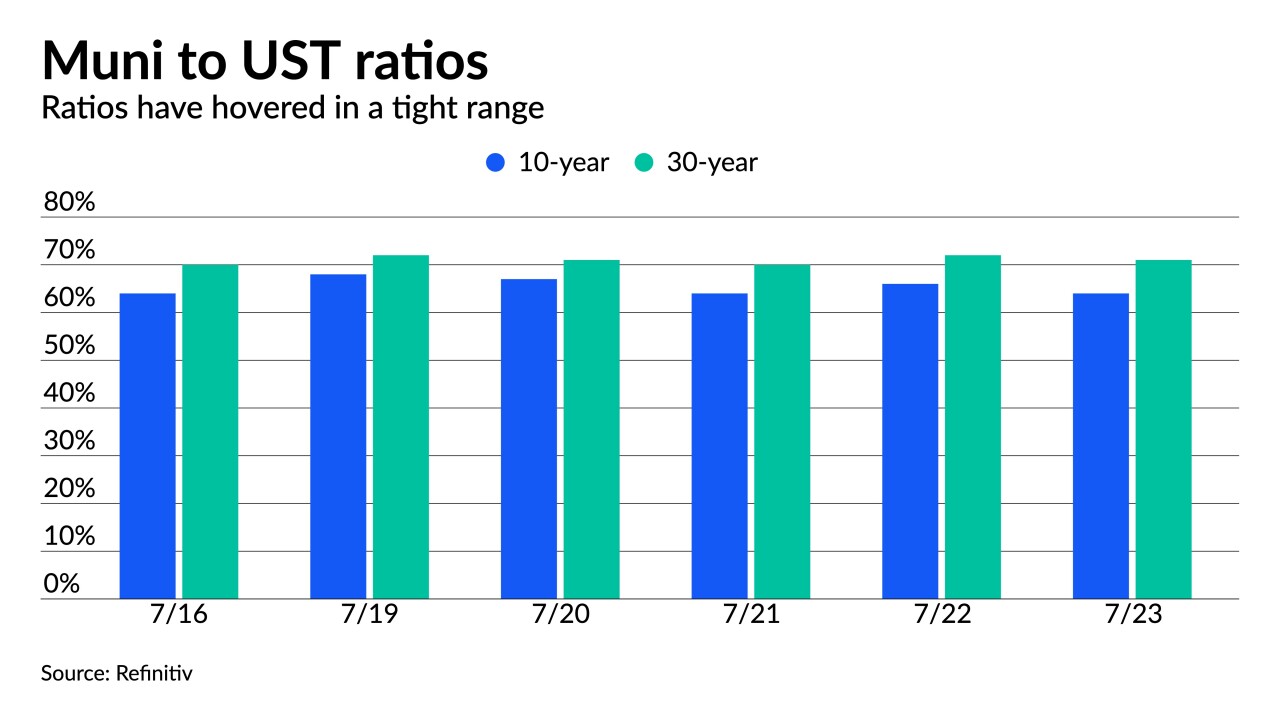

The last week of July marks a lighter calendar while August redemptions are huge compared to the expected supply. Investors need to get in line and likely accept lower yields and continued historically low ratios.

July 23

-

Low ratios, low yields and massive demand are leading to a market that is mostly on its own. Refinitiv Lipper reported $1.7 billion of inflows.

July 22

-

Whether a BABs-like program could make it into actual law in Washington is still highly uncertain. What is certain: Some form of infrastructure spending is must-pass legislation because federal-aid highway funding is set to expire in October.

July 22

-

The rating agencies affirmed two AA-plus and one triple-A rating ahead of the deal.

July 22

-

The larger new issues and aggressive swings in taxables had investors on guard as triple-A curves were pressured outside 10-years, but the asset class still vastly outperformed UST while ICI reports nearly $3 billion more inflows.

July 21

-

Negotiated deals were repriced to lower yields while competitive deals saw levels coming in through triple-A benchmarks. High-grade benchmarks were little changed.

July 20

-

Wednesday will be the first Senate vote on advancing a bipartisan infrastructure deal.

July 20

July 20

-

The prominent Chicago health system's refunding will simplify its debt structure, cut interest rates, and provide longer-term fixed financing.

July 20

July 20

-

Municipal triple-A benchmarks were pushed to lower yields by one to three basis points across the curve, with the bigger moves out long, but still vastly underperformed the 10-plus basis point moves in UST.

July 19

-

Issuers should recognize their ability to prepay debt is an extremely important term, and they should consult with their MAs to achieve the most liberal prepayment term consistent with the type of financing they are doing.

July 19 McNees Wallace & Nurick

McNees Wallace & Nurick