-

Municipals were unchanged for the fourth consecutive day this week amid slight Treasury strength as demand for yield continued.

August 19

-

Demand was brisk in the primary market while the short-term market traded sideways on the pressure from the heavy new issue calendar, the release of the FOMC minutes and Treasury auction.

August 18

-

The Puerto Rico Aqueduct and Sewer Authority sold $813 million of senior lien revenue bonds consisting of tax-exempt refunding, taxable refunding and forward delivery refunding bonds.

August 17

-

As New York City launched the first of its two-day retail order period on $1.039 billion of GO bonds, the market was uneventful ahead of $9.76 billion in the primary market this week

August 16

-

The short end of the muni market saw trading of larger blocks at or below benchmarks but yield curves were little changed on a summer Friday.

August 13

-

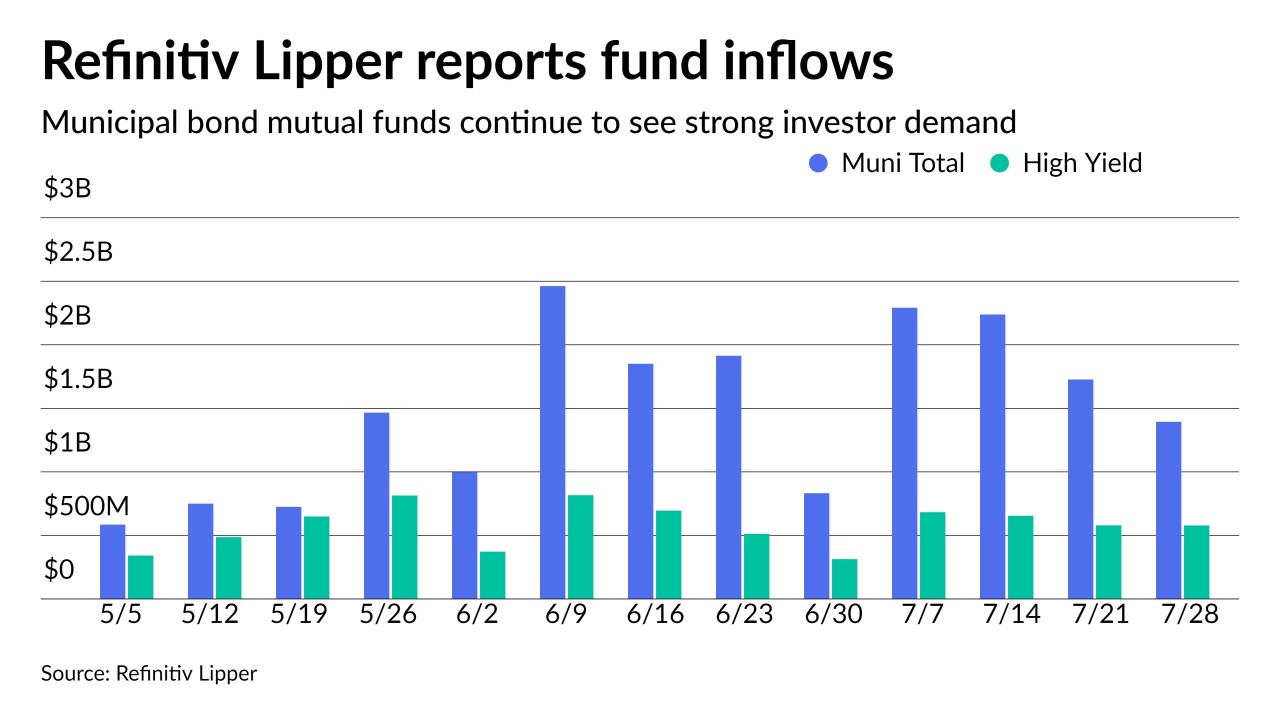

Refinitiv Lipper reported $1.87 billion inflows. A solid demand component for the market, but some suggest the move into bonds from equities is more an asset reallocation than investors keen on fixed income.

August 12

-

Another $2 billion-plus was reported flowing into municipal bond mutual funds in the latest week, continuing to be a supportive demand component for munis.

August 11

-

The increasing influence of institutional market participants is even stronger in the taxable muni sector, a Municipal Securities Rulemaking Board report finds.

August 11

August 11

-

Municipals are tethered to Treasuries, more so in recent sessions, and have cheapened, but strong technicals — $18.5 billion of net negative supply and large reinvestment needs — still hang overhead.

August 10

-

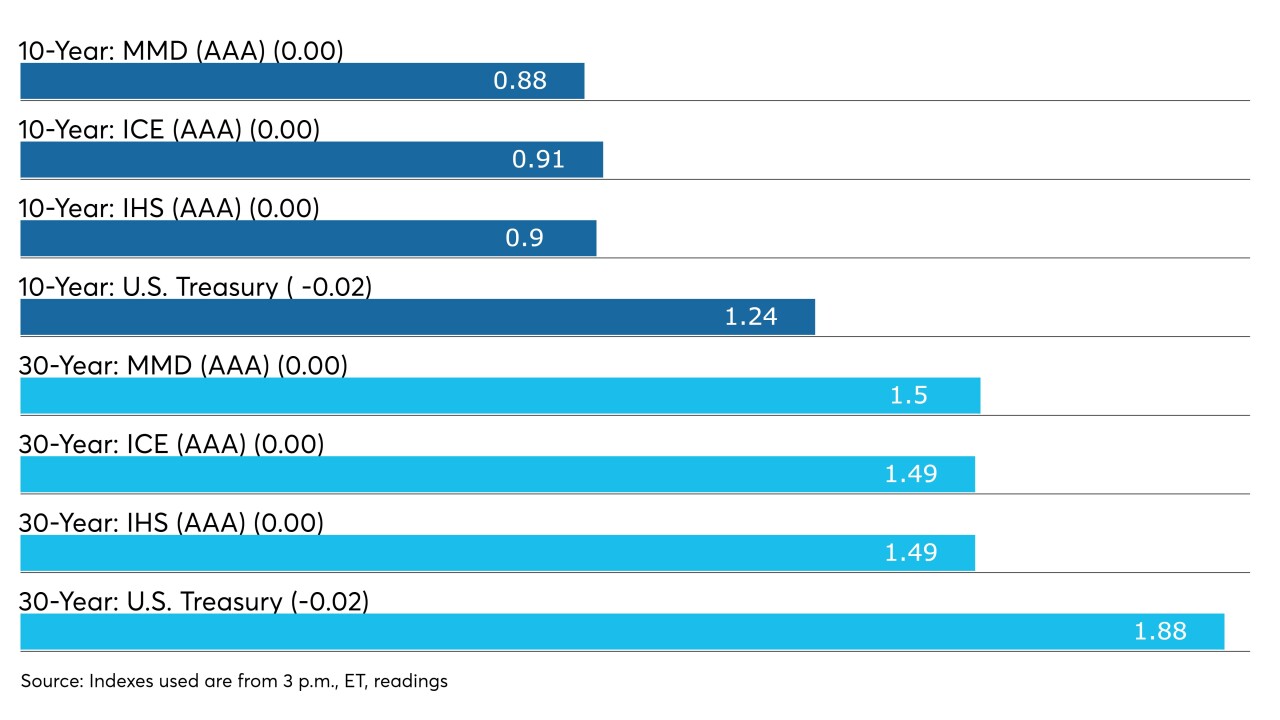

Triple-A benchmarks saw cuts of one to two basis points across the curve, but still outperformed two days of UST weakness and have outperformed UST losses since the start of the month.

August 9

-

Better-than-expected job gains, a rising UST complex and an increase in supply to test municipals' resolve.

August 6

-

Secondary trading petered off into Thursday afternoon, holding triple-A benchmarks steady as most participants await Friday's nonfarm payrolls.

August 5

-

The firm has brought on Kalotay Analytics' quantitative libraries to calculate certain metrics, including average life dates and cash-flow yields for taxable term bonds.

August 5

-

The short end of the market has little room to fall lower.

August 5

-

With all eyes on Friday’s employment report, since several additional strong months of gains are needed for the Federal Reserve to be comfortable announcing a tapering of its asset purchases, Wednesday’s news could signal trouble.

August 4

-

Effective spread data yielded interesting results about the way corporate and municipal bonds were treated by Fed backstop programs.

August 4

August 4

-

Tighter bidding on bonds 10 years and in pushed high-grade benchmark curves to bump yields.

August 3

-

Municipals returned 0.83% in July with a year-to-date return of 1.90%. High-yield returned 1.20% in July and 7.40% year-to-date. Taxables led July with 1.65% returns and 1.95% for the year.

August 2

-

Muni participants await a new month with growing issuance, but perhaps not quite enough as issuers are hesitant to add more debt before final word from Washington on infrastructure.

July 30

-

Washington GOs came at tighter spreads than a spring sale in the competitive market while sizable negotiated deals saw bumps in repricings. Refinitiv Lipper reported $1.4 billion of inflows in the 21st consecutive week.

July 29