-

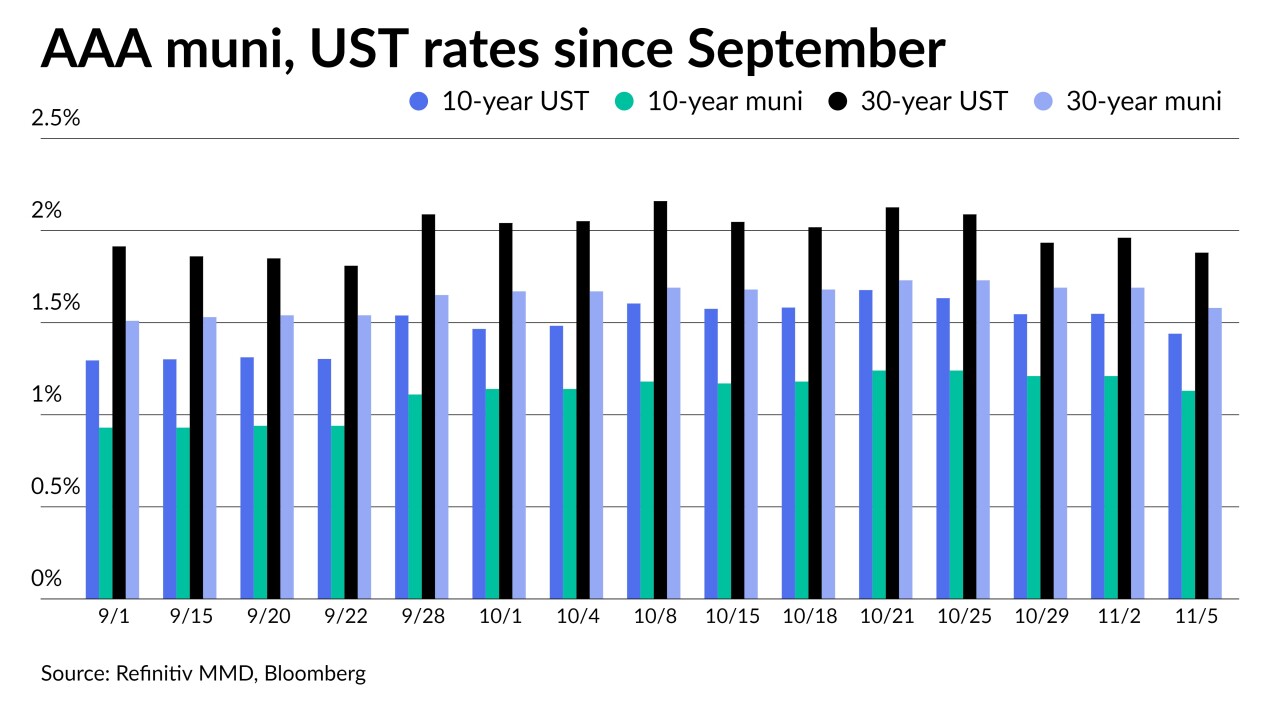

The long end of the municipal curve rallied under a backdrop of stronger-than-expected October jobs data and upward revesions to the prior two months ahead of the arrival of $9.6 billion next week.

November 5

-

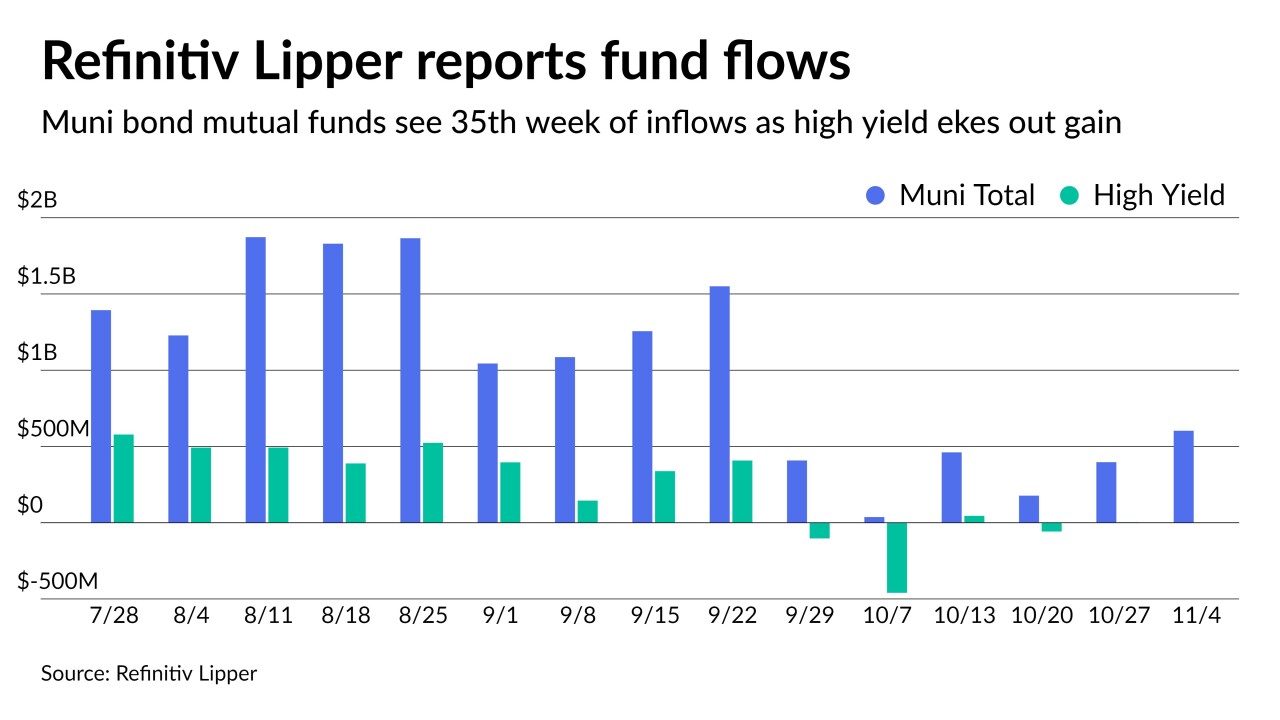

For 35 weeks in a row, investors have put cash into municipal bond funds as Refinitiv Lipper reported $603 million of inflows while high-yield funds eked out a gain of slightly more than $1 million.

November 4

-

After the FOMC made taper official, high-grade benchmark yields ended the day one to three basis points better while USTs ended the day higher after an up-and-down trading session that moved the 30-year back above 2%.

November 3

-

The FOMC will likely take the opportunity to profess its reliance on data to decide liftoff and reiterate the threshold for a rate hike remains higher than for taper.

November 2

-

Chuck Stavitski and Elaine Brennan of Roosevelt & Cross and Ken Bieger of the Niagara Falls Bridge Commission talk about how the Canadian border closing due to COVID-19 affected upstate New York issuers. Chip Barnett hosts. (16 minutes)

November 2

November 2

-

Though monetary policy has been in the forefront, at mid-month the tone changed with global inflation outlooks and federal infrastructure and social package in flux.

November 1

-

A lighter, $5 billion calendar, heavy on healthcare, kicks off November. Most participants agree volatility in U.S. Treasuries will be a leading factor for municipal market performance. Uncertainty in Washington also isn't helping the asset class.

October 29

-

Amid a flattening municipal yield curve and inversion of the Treasury market, new issues fared better than the secondary on Thursday as participants prepared for month end.

October 28

-

ICI reported the lowest inflows since outflows in March, while exchanged-traded funds saw an uptick.

October 27

-

As of now, returns for the month will very likely end in the red. The Bloomberg U.S. Municipal Index is at -0.40% for the month and +0.39% for the year.

October 26

-

Despite a short-end U.S. Treasury rally, municipals face pressure on the one- and two-year as participants look to month-end positioning.

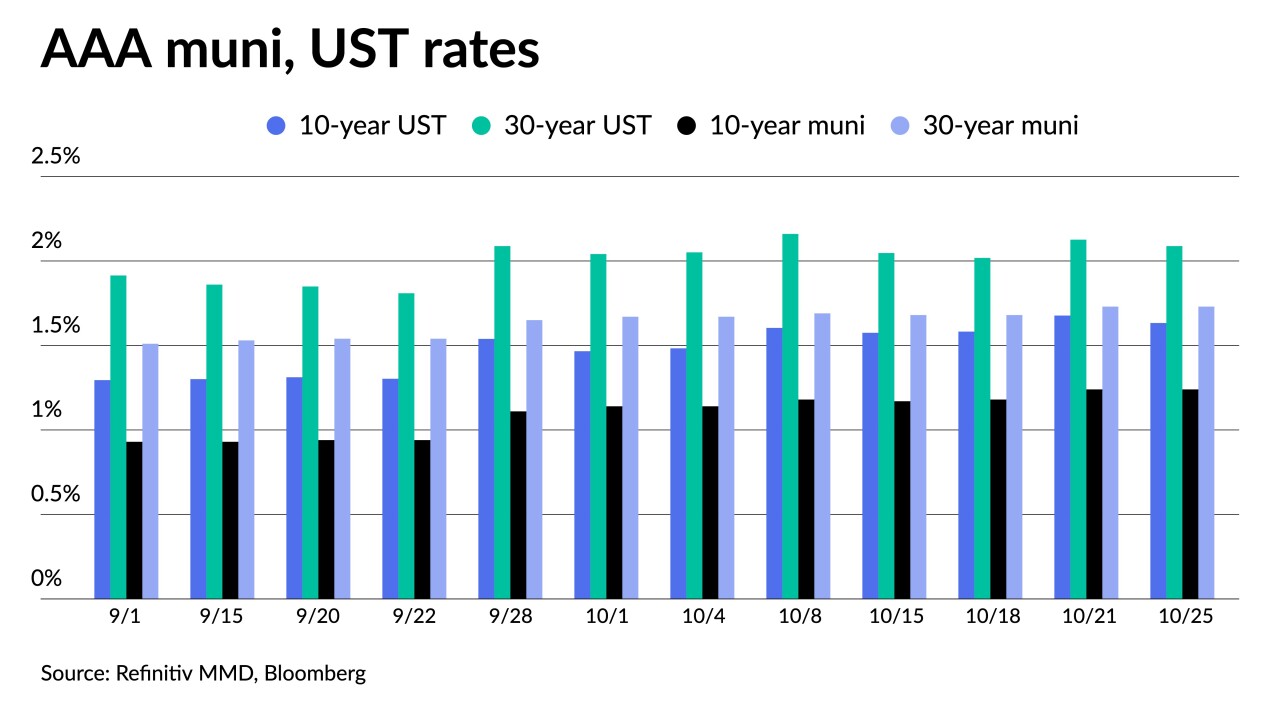

October 25

-

Volume falls slightly in the week of October 25 with total potential volume estimated at $7.408 billion: $6.036 billion of negotiated deals and $1.372 billion in the competitive market.

October 22

-

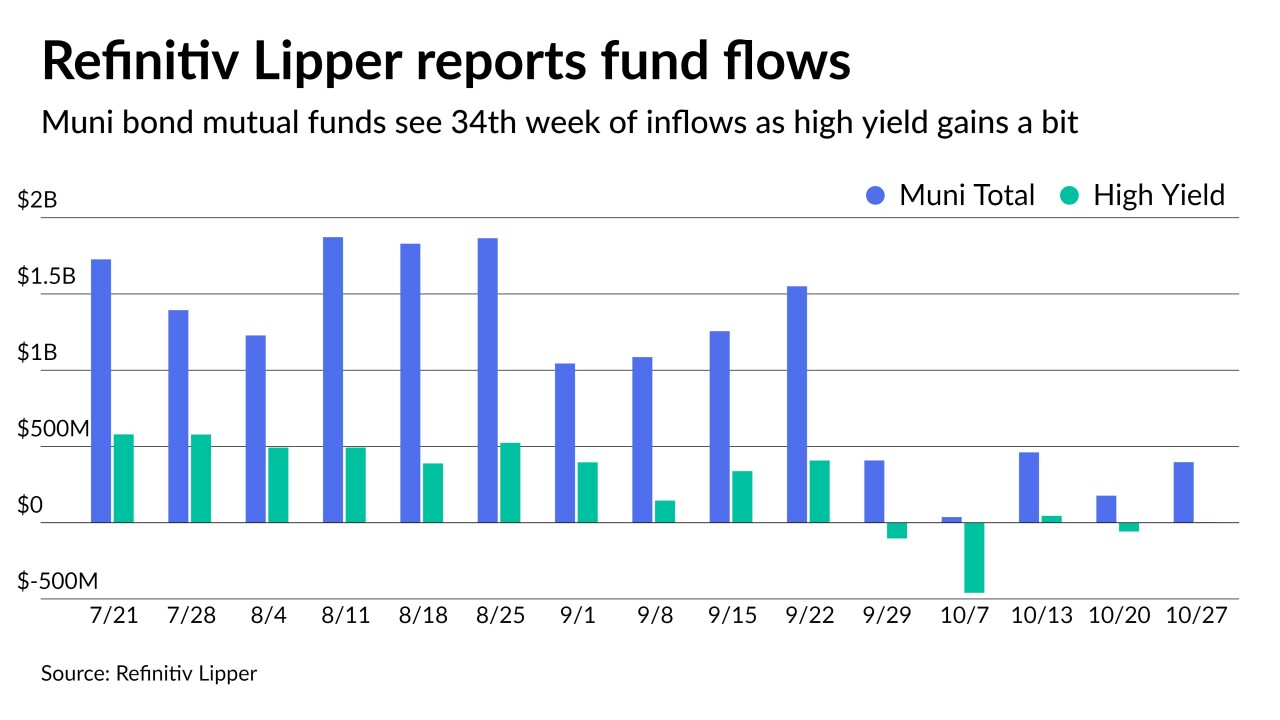

Municipal bond mutual fund inflows fell to $177 million while high-yield is back to outflows, both signaling selling may be moving the market toward another larger correction.

October 21

-

The Investment Company Institute reported $385 million of inflows while ETFs fell to $124 million.

October 20

-

Spreads have been widening, but secondary trading was on the light side and triple-A benchmarks were cut by only a basis point in spots even as U.S. Treasury yields once again rose on the 10- and 30-year.

October 19

-

Triple-A benchmarks saw one basis point cuts in spots inside 10 years while the five-year U.S. Treasury hit a high of 1.154%.

October 18

-

Friday’s data suggested inflation remains a problem, as the voices calling for Federal Reserve action increase.

October 15

-

Municipals have mostly held steady as bid-wanteds have risen, but so have yields and ratios, making for a more satisfactory range for investors getting into the market at these new higher levels.

October 14

-

Another round of inflows was reported from the Investment Company Institute — the 31st consecutive week — but they came in at $308 million for the week ending Oct. 6, the lowest since outflows in March.

October 13

-

Volatility in the U.S. Treasury market continues to pull on municipal bond valuations, despite little trading volume.

October 12