-

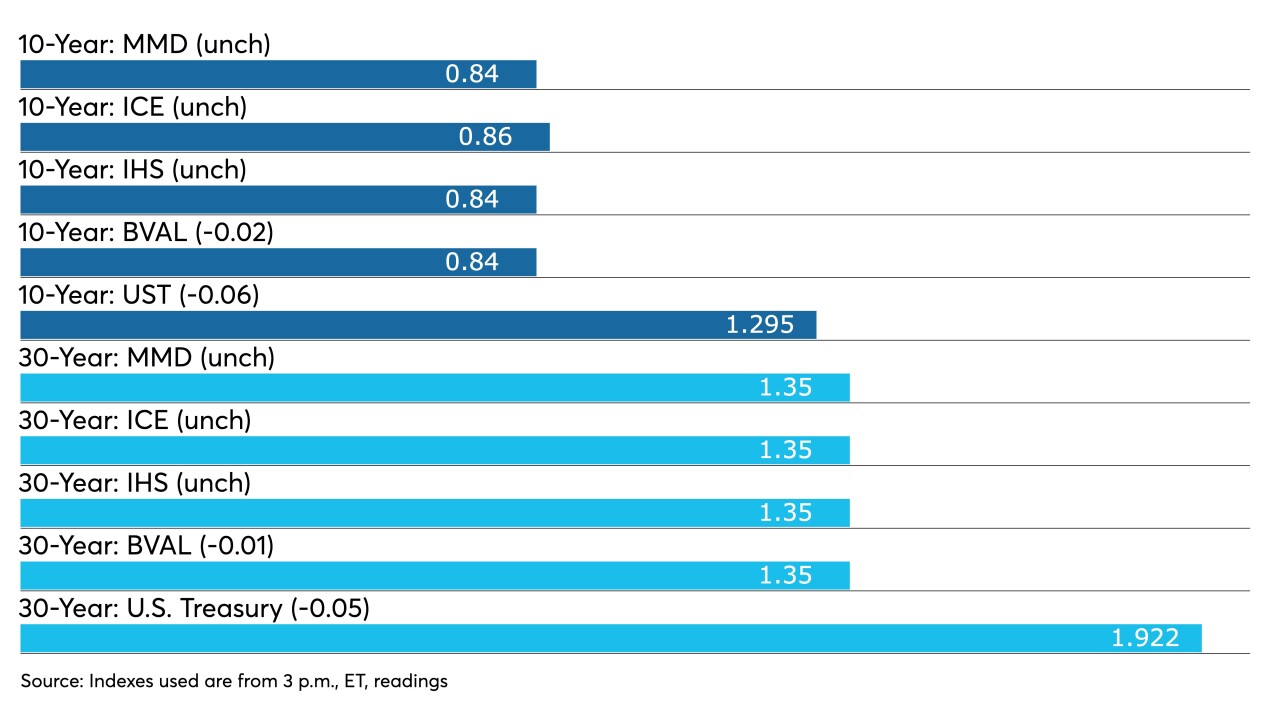

With municipal yields at exceedingly low absolute levels, the spread tightening between credits also continues.

July 26

-

The pilot program aims to expand its all-to-all Open Trading marketplace by allowing investor clients to select a diversity dealer to intermediate in secondary trading.

July 26

-

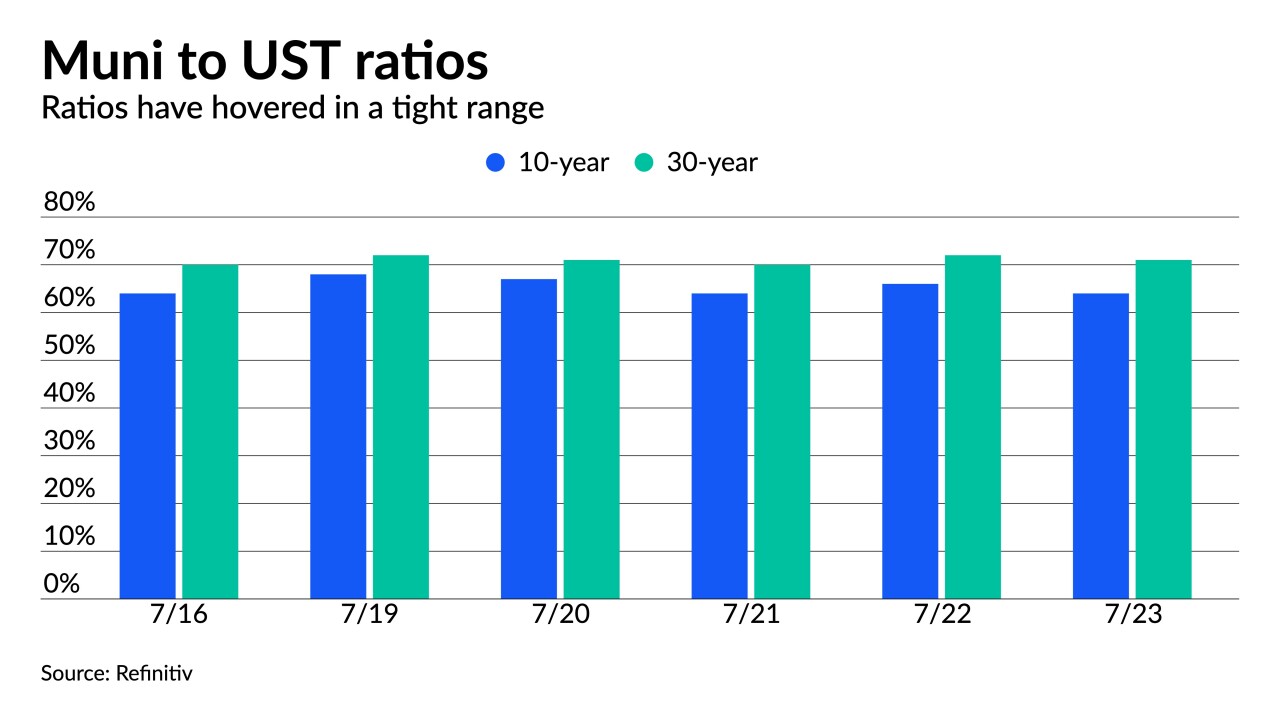

The last week of July marks a lighter calendar while August redemptions are huge compared to the expected supply. Investors need to get in line and likely accept lower yields and continued historically low ratios.

July 23

-

Low ratios, low yields and massive demand are leading to a market that is mostly on its own. Refinitiv Lipper reported $1.7 billion of inflows.

July 22

-

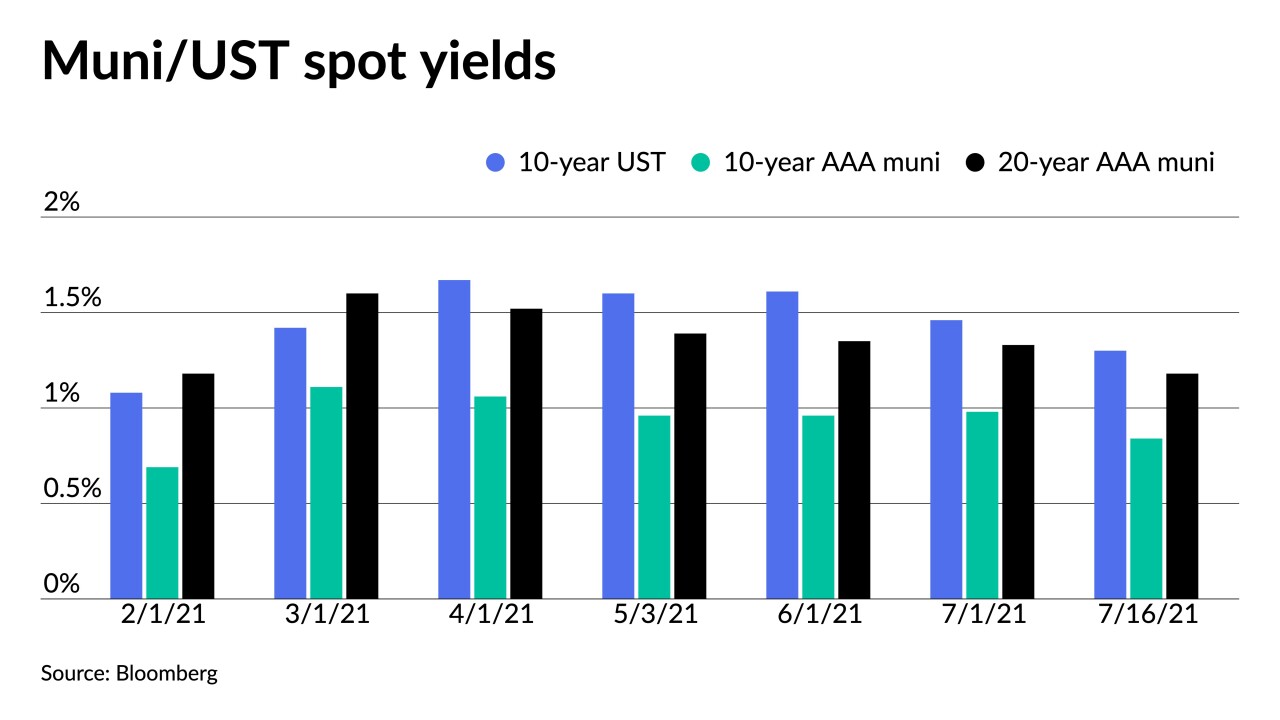

The larger new issues and aggressive swings in taxables had investors on guard as triple-A curves were pressured outside 10-years, but the asset class still vastly outperformed UST while ICI reports nearly $3 billion more inflows.

July 21

-

Negotiated deals were repriced to lower yields while competitive deals saw levels coming in through triple-A benchmarks. High-grade benchmarks were little changed.

July 20

-

Municipal triple-A benchmarks were pushed to lower yields by one to three basis points across the curve, with the bigger moves out long, but still vastly underperformed the 10-plus basis point moves in UST.

July 19

-

Supply, however, is still less than the massive amounts of cash on hand. Bond Buyer data shows 30-day visible supply at $12.53 billion.

July 16

-

U.S. Treasuries have been volatile the past five sessions, with municipals largely ignoring the ride. Participants mostly have accepted current rates and ratios as large amounts of cash slosh around a market with strong technicals.

July 15

-

Perform, a portfolio management platform for institutional investors who want to accesses the municipal bond market, will be integrated into ICE Bonds.

July 15